Artea Bank 2026 Q1 financial review

Down, but not the worst

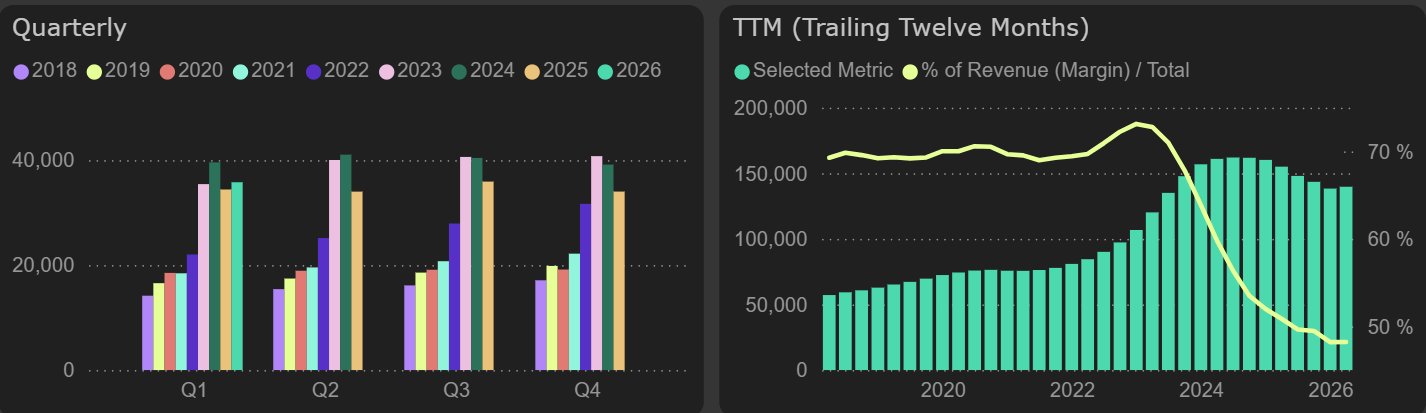

Artea Bank’s results for the first quarter of 2026 appear average in the context of other banks. The bank reported net profit of €15.4M for the quarter, down 13% YoY (-€2.3M). By comparison, Coop Pank delivered profit growth (+5% YoY), while LHV Group saw a much sharper decline (-32% YoY).

Net profit

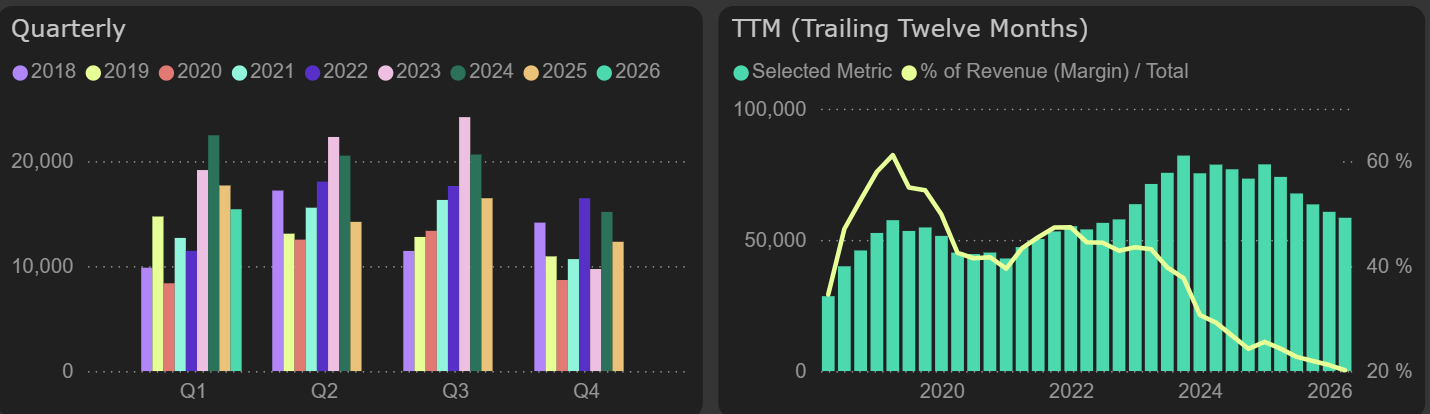

The dynamics of net interest income at Artea Bank were positive this quarter – although growth was not rapid, it reached 4%. Coop Pank showed stronger growth at 9%, whereas LHV Group, in contrast, recorded a 4% decline.

Net interest income

It’s worth noting that in Q1 last year, Artea Bank’s result benefited from non-core items: a €3.6M higher gain from the derecognition of financial assets and €1.3M lower trading losses (including insurance activities) compared to this year.

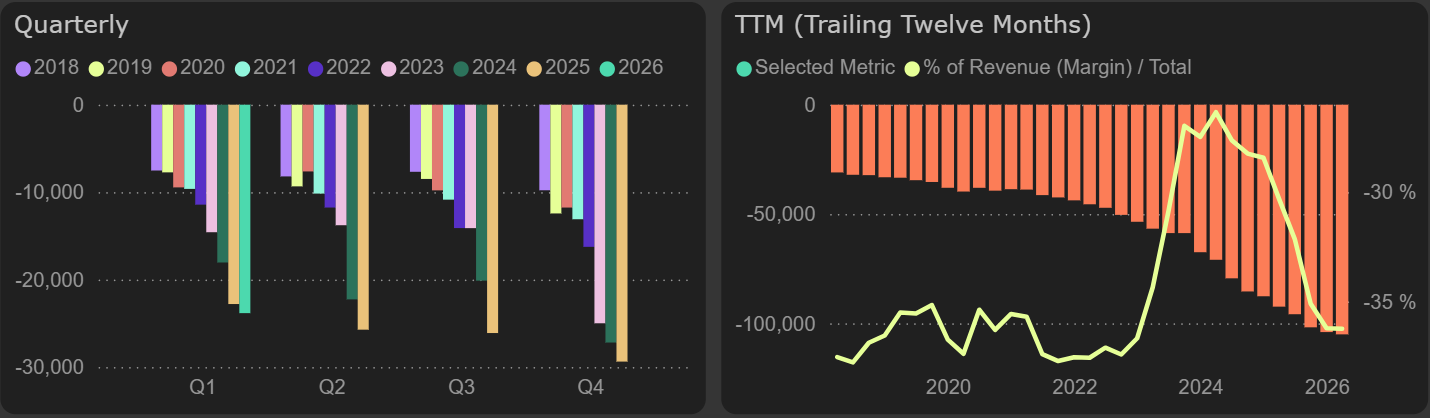

Other operating expenses rose by 10%, putting pressure on performance. On the positive side, employee-related costs in Q1 remained largely stable.

Staff and other operating expenses

Profit before impairment losses this quarter was 18% lower than last year. However, due to lower impairment losses, the pressure on the final result was smaller.

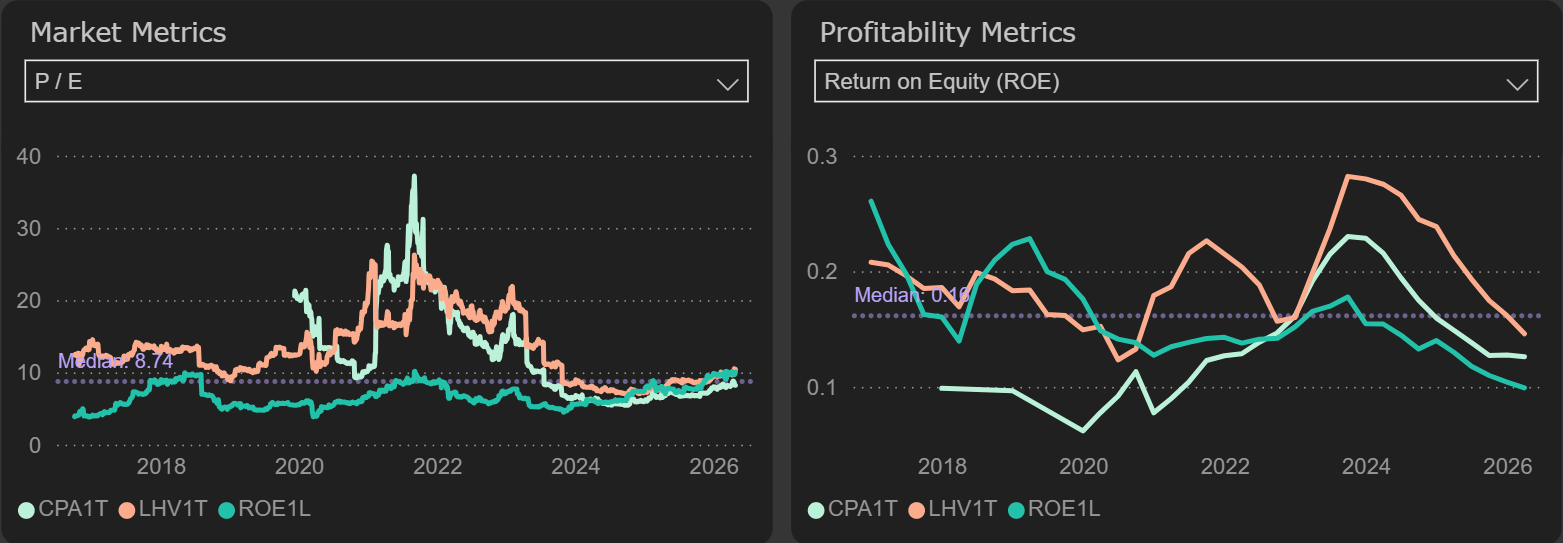

Based on valuation metrics, Artea Bank remains fairly neutral. Coop Pank stands out with a lower P/E, a similar P/BV, and a higher ROE. LHV Group still trades at a premium, although its P/E gap versus Artea is relatively small. While LHV continues to lead in ROE, the gap versus peers – particularly Coop Pank – has been narrowing recently.

Trends in banks P/E and ROE ratios