Grigeo Group 2026 Q1 financial review

Growth meets margin pressure

Grigeo Group's margins continued to decline in the first quarter of 2026, resulting in an opposite profit trend despite revenue growth.

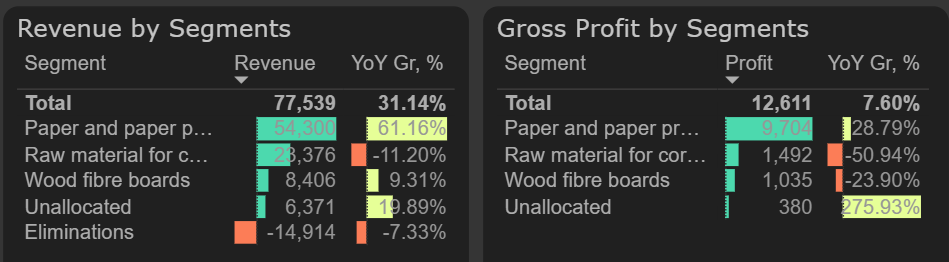

Revenue in the first quarter of 2026 was 31% higher than a year ago, reaching €77.5M. As expected following the acquisition of the company, revenue in the paper segment increased by 61%. Although revenue in the wood fibre boards segment also grew (+9% YoY), the raw material for corrugated cardboard and related production segment moved in the opposite direction, with revenue declining by 11% YoY.

Results by segments, 2026 Q1

All of the company's segments faced profitability challenges this year. In the paper segment, gross profit increased, but due to a contraction in margin, its growth rate was almost half the pace of revenue growth, reaching 29% YoY. Meanwhile, gross profit in the other segments declined. Overall, gross profit increased, but at a significantly slower pace than revenue — only 8% YoY.

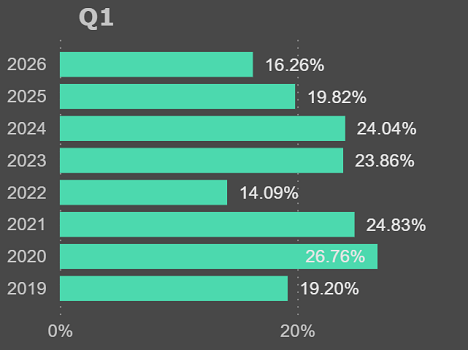

Q1 gross margin

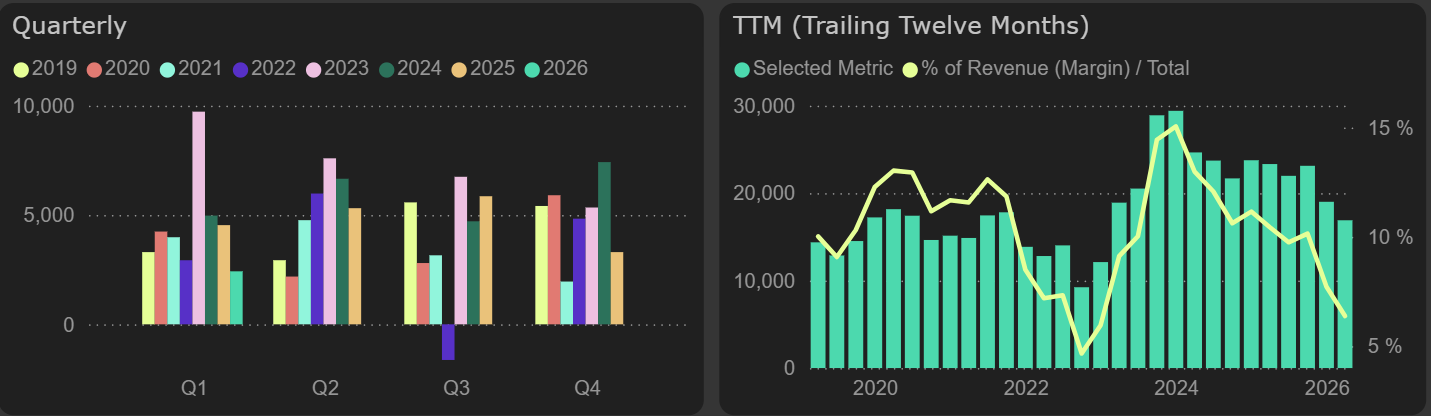

In the first quarter of 2026, administrative expenses grew broadly in line with revenue, rising by 33% YoY. However, additional pressure on margins came from selling and distribution expenses, which were 46% higher than a year ago. As a result, profitability declined — EBITDA fell by 21% YoY, while operating profit contracted even more sharply, decreasing by 47% YoY to €2.4M.

Operating profit

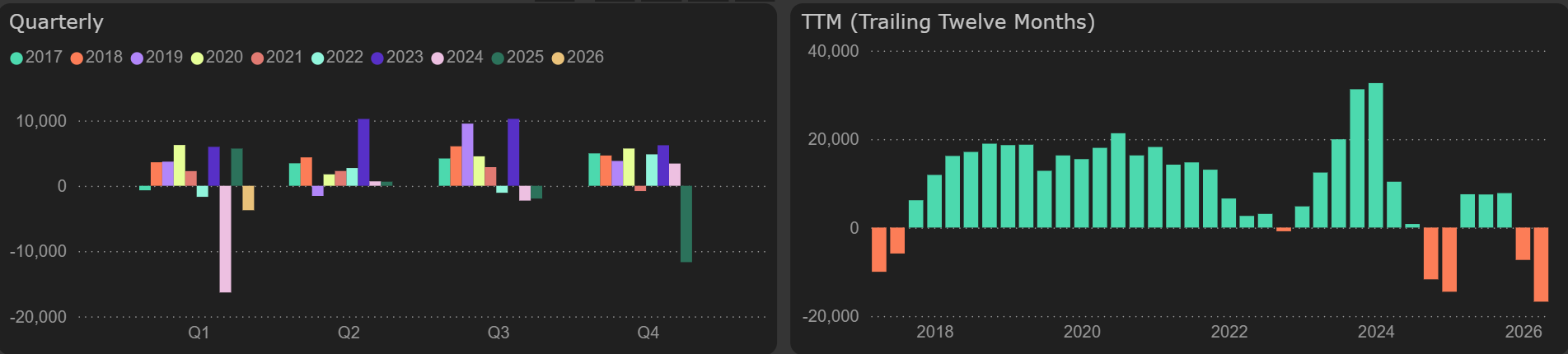

Free cash flow remained negative both for the first quarter and on a trailing twelve-month basis. This quarter, funds from operations declined by 29% YoY to €5.1M, while high investments in long-term assets nearly doubled that amount, reaching €10.4M.

Free cash flow

Valuation metrics moved higher: P/E increased to 9.7x and EV/EBITDA to 4.9x, although the latter remains relatively low.