Ignitis Group 2026 Q1 financial review

Top-line growth didn’t reach the bottom line

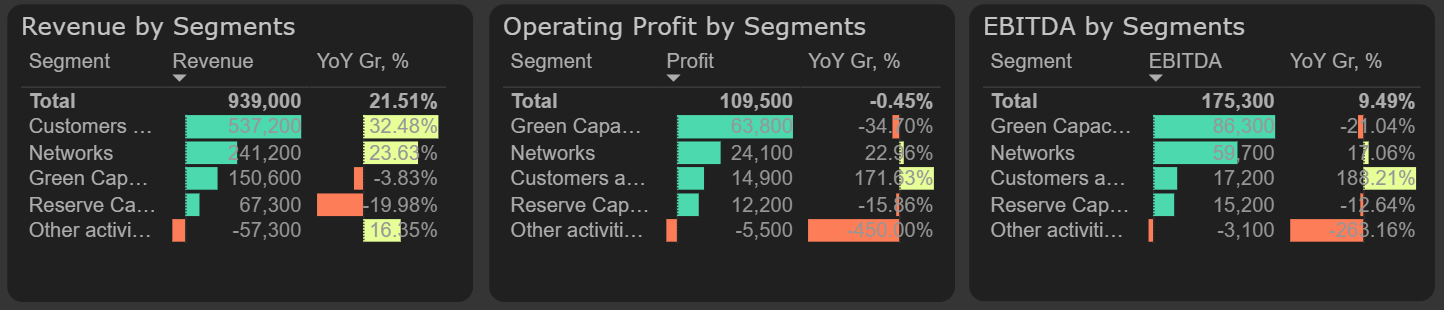

Ignitis Group revenue increased 22% YoY to €939M. Both revenue and profit grew in the Customers & Solutions and Networks segments, while results in the Green Capacities and Reserve Capacities segments weakened.

Results by segments, Q1 2026

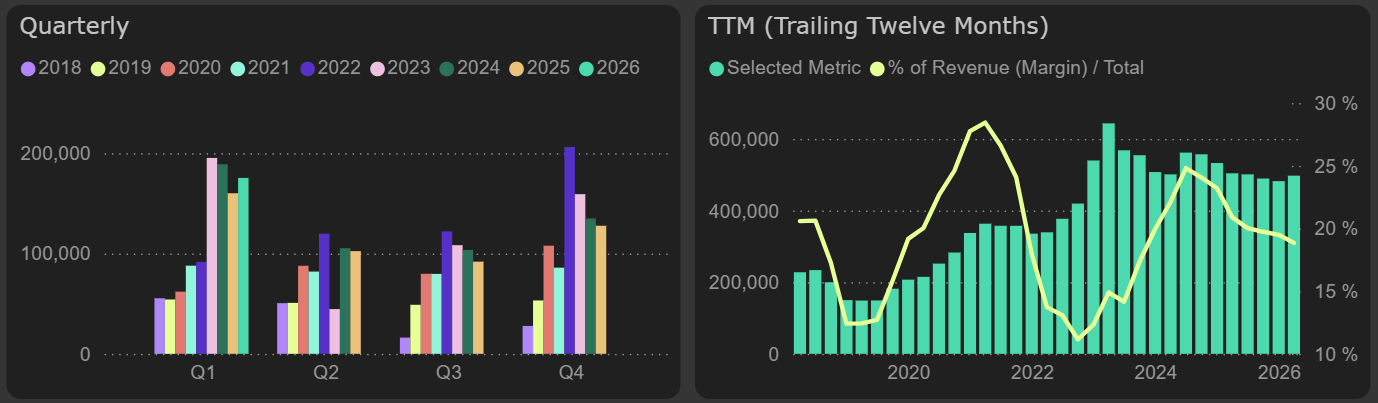

EBITDA grew slower than revenue, increasing 10% YoY to €175.4M. EBITDA margin came under pressure from a 25% rise in purchases of electricity, natural gas and other services, while all other operating expenses increased at a slower pace of 20%. The strongest margin pressure was recorded in the Green Capacities segment, where EBITDA margin declined from 70% in Q1 2025 to 57% in Q1 2026.

EBITDA

Growing non-current assets led to a significant increase in depreciation expenses, which rose 29% YoY. This offset growth at the operating profit level.

The trend in adjusted results was weaker: adjusted EBITDA increased only 2% YoY, while adjusted EBIT declined 9% YoY.

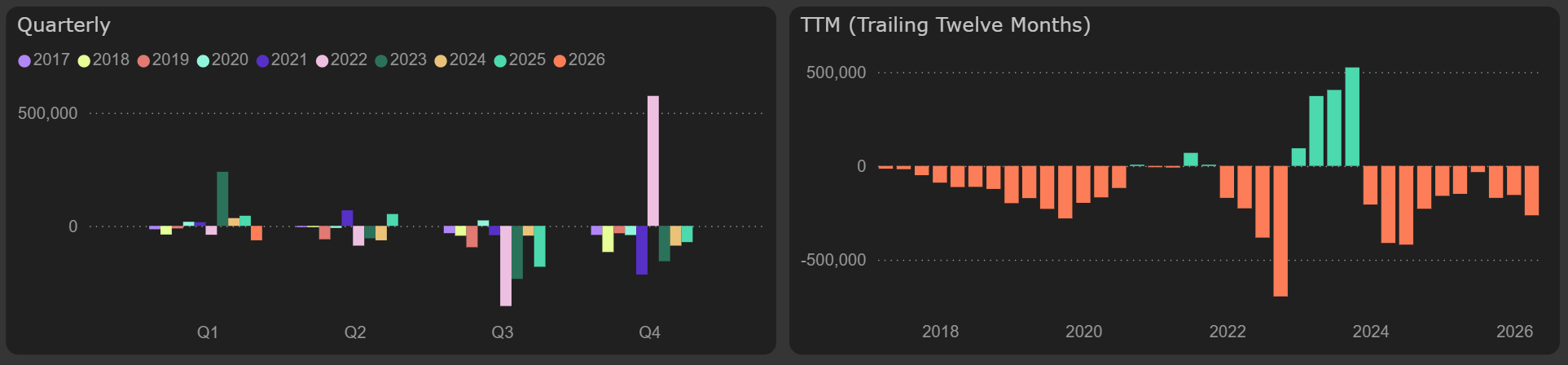

Financial activity results were significantly weaker this quarter due to negative foreign exchange effect (compared to a positive result a year ago) and higher interest expenses. As a result, net profit declined 13% YoY to €73M.

Net profit

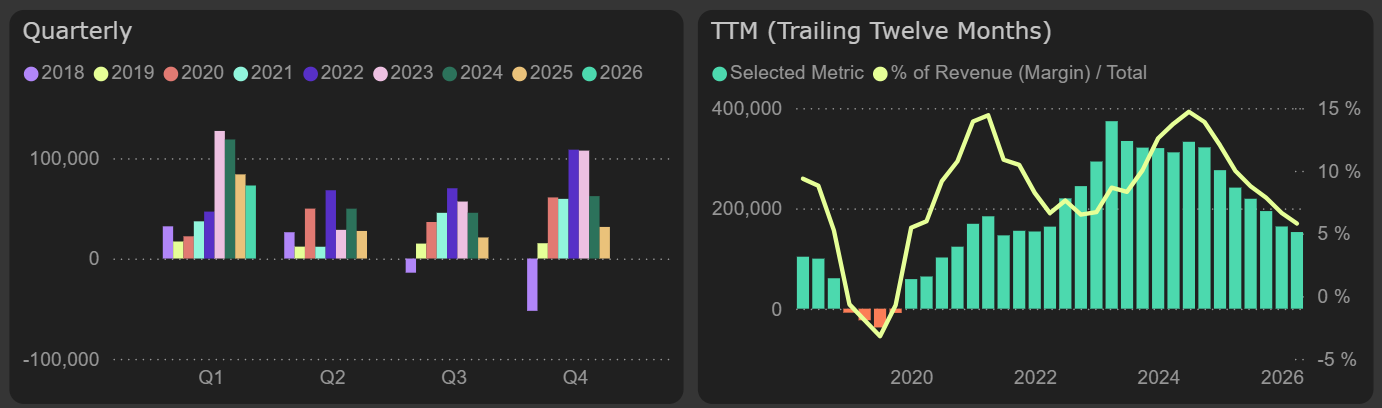

Cash flow trend remain unchanged – free cash flow stayed negative. Q1 FFO of €160M was not sufficient to cover €166M of investments in non-current assets and €60M of working capital needs.

Free cash flow